Car Shopping? Let Me Help.

Enter Your VIN

Get your vehicle report in seconds

Comprehensive History

Get detailed accident records, title information, and service history.

Buy or Avoid Verdict

Get a clear recommendation based on the vehicle's history and condition.

Market Comparison

See how this vehicle compares to similar models in pricing and reliability.

Always Check the History Before Buying.

$9.99. No Hidden Subscriptions. Check it Out:

2020 Honda Civic EX

VIN: 1HGFAKEVINNUMBER123 (DEMO)

VIN

1HGFAKEVINNUMBER123

Year

2020

Make

Honda

Model

Civic

Trim

EX

Body Style

Sedan

Engine

1.5L Turbo I4 174hp

Drivetrain

FWD

Transmission

Continuously Variable Transmission (CVT)

Vehicle History Highlights (Demo Data)

1 Record Found

Based on available records

1 Record Found

Based on available records

1 Open Record

Based on available records

35,000 Miles

User provided (Demo)

38,000 Miles

Based on KBB typical mileage (Demo)

3 Records Found

Based on available records

Key Issues to Consider (Demo Data)

Accident History Found

This vehicle has 1 reported accident(s)/damage record(s). Review the history section for details.

Total Loss Record Found

This vehicle has been reported as a total loss. This may impact value and insurance. Review history.

CarReport Score

This score reflects the vehicle's overall quality based on accident history, ownership, recalls, mileage, market value, and safety ratings.

Key factors: Severe accident history, Major recall issues, Many owners

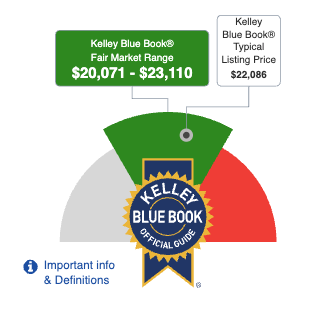

Price Analysis

Kelley Blue Book® Fair Purchase Price

$21,591

The price others typically pay based on actual transactions

Listing Price

$28,000

HIGH PRICE

This vehicle is priced above the KBB Fair Purchase Price.

This suggests the price may be higher than what others typically pay for similar vehicles.

Mileage History

Ownership Timeline (Demo Data)

Title Issued

Location

CA

Title Issued

Odometer Reading

15 miles

Details

CA DMV title record

Additional Information

Mileage reported in miles

Current Title

Location

CA

Current Title

Odometer Reading

18000 miles

Details

CA DMV title record

Additional Information

Mileage reported in miles

Salvage/Total Loss Record

Location

123 Main St

Details

Reported as Sold by Insurance Company

Additional Information

Reported by: XYZ Insurance

Location: 123 Main St, Anytown USA

Vehicle Color: Gray

No export intended

📞 555-1234

Towed or Impounded

Vehicle was towed due to parking violation

Location

Los Angeles, CA

Additional Details

Towed by: City Parking Enforcement

Reason: Parking violation

Location: Downtown LA

Additional Information

Vehicle was towed due to parking violation

Current Title

Location

NV

Current Title

Odometer Reading

34000 miles

Details

NV DMV title record

Additional Information

Mileage reported in miles

Open Recall - Airbag Inflator

Details

Airbag inflator may rupture, increasing risk of injury. Recall open.

Towed or Impounded

Vehicle was impounded by law enforcement

Location

Las Vegas, NV

Additional Details

Impounded by: Las Vegas Police Department

Reason: Investigation hold

Location: Central Impound Lot

Additional Information

Vehicle was impounded by law enforcement

What Our Users Say

"Found out the truck I was gonna buy had 3 owners including a fleet. Didn't know that till I got the report. $10 saved me big time."

2019 Ford F-150

"Used this to compare a few cars. Ended up getting the one with the highest score and paid less than it was worth. So easy to read too."

2016 BMW 328i

"Used this for my daughter's first car. It showed a recall and helped us pick a better one. Simple layout, no junk info."

2021 Honda CR-V

Only $9.99

for a vehicle history report

No hidden fees. No subscriptions. Just a one-time payment for your peace of mind. Enter your VIN to get started!

*Price is for a single, full vehicle history report. No recurring charges.

Enter Your VIN

Get your vehicle report in seconds